Helio taps Obopay for mobile payments

Chalk another MVNO up for Obopay: After announcing an expected deal with Amp'd Mobile, Obopay has signed one with MVNO Helio for its mobile payments service. Just like the Amp'd offering, Obopay will enable Helio subscribers to use its "real-time, secure, mobile peer-to-peer payment service, which is linked to an Obopay Prepaid MasterCard account." The service allows users to check balances, view payment histories, add funds and more.

For more details on the Helio-Obopay tie-up:- read the company press release

Thursday, December 21, 2006

Tuesday, December 19, 2006

African mobile payments - 160 Characters

m-Payment: African Virtual Pre-Pay By SMS

| Submitted by Mike Grenville on Tue, 12 Dec 2006 11:36 |

Text messages are helping resellers replace scratch cards in Africa and South America.

Africa has the quickest growth rate in pre-pay communication, over and above any other region in the world apart from Eastern Europe. Africa had more than 60 million pre-pay subscriptions at the end of 2003 increasing to 100 million in 2005, nearly doubling the size of the market in just two years.

For GSM operators in Africa, as well as in Asia and Latin America, 75-90 per cent of their revenue comes from pre-pay. In these places, few people have credit cards or bank accounts and so scratch cards are mostly used to top up credit. However, as well have having distribution problems to remote areas, they are also vulnerable to theft.

XIRING believes that the pre-pay communication solution that they have developed, in conjunction with Expand, will provide operators with a secure and flexible way to resell credit.

All the operator has to do is provide the merchant with a time credit, which is uploaded onto a smart card and inserted into a mobile XIRING reader. After inserting the correct PIN code, recharge numbers are generated which can then be resold o mobile phone users. The user then sends a SMS to the operator with the recharge code and receives a SMS in return with their time credit.

There are two styles of offline card readers - one small and other like PDA size which can connect to small printer as required legally in some countries.

Roger Mechri,(pictured) International Indirect Sales Manager, XIRING comments: “This type of pre-pay solution is particularly valuable in the developing world, such as Africa, where there is an absence of telecommunications infrastructure and where there are very few cash points and even fewer people with bank accounts. The mobile pre-pay technology allows GSM operators to increase their distribution channels, reaching a much larger network of people, even those individuals in the more deprived regions."

“This virtual pre-pay solution also provides greater security allowing operators to get rid of scratch cards and the associated problems of control and distribution. Africa has the quickest growth rate in pre-pay communication, over and above any other region in the world apart from Eastern Europe. Africa had more than 60 million pre-pay subscriptions at the end of 2003 increasing to 100 million in 2005, nearly doubling the size of the market in just two years.”

Launched February 2006, so far three companies are using the solution in Africa; MTN Nigeria has 5,000 terminals distributed, Nginge Boke 2,000 terminals in South Africa, Expand in Seychelles and in South America Umbryo in Brazil is running a pilot. Discussions are progressing with two operators in Madasgascar - Orange & Madagascar Telecom.

"The technology is encouraging an entrepreneurial spirit amongst small businesses keen to distribute the solution, thereby helping to stimulate the local economies in Africa" said Mechri.

Friday, December 15, 2006

Barclays Oyser Card - ePaymentNews

Barclays to Add London Transit to Contactless Cards

Transport for LondonOyster is a prepaid contactless smart card that contains London transit tickets. Since Oyster was launched in 2003, 6 million cards have been issued to Londoners. Oyster cards can be topped up over the Internet, by phone or at a ticket office. One of the UK's top five banks, Barclays has signed an agreement with TranSys, which runs the Oyster card scheme on behalf of Transport for London (TfL), the capital's transit authority. The deal gives Barclays exclusive rights to place Oyster on contactless Barclaycard credit cards and Barclays Connect Visa debit cards for the next three years. Barclays says its contactless credit and debit cards will contain EMV chip-and-PIN technology. For transactions over £10 (US$19.70), cardholders will need to swipe their cards and enter a PIN. However, for payments under that amount, cardholders will simply wave their cards in front of a contactless reader, Barclays says. Following a trial in February 2007 involving Barclays, Visa, TranSys and TfL, the first Barclaycards and Barclays Connect cards to include Oyster will be issued in mid-2007, Barclays says. Barclays is the first UK bank to commit to launching contactless cards, although Royal Bank of Scotland has been trialing contactless cards at its Edinburgh head office. Last month, Visa UK announced that its member banks had agreed to roll out contactless cards across Britain, starting in London, by the end of next year.

www.barclaycard.co.uk

Barclays news release

Transport for London website

Visa UK Plans Contactless Rollout in 2007

MasterCard Announces European Contactless Trials

RBS Says Contactless EMV Trial a Success

Transport for London

Dec 14 2006 : Barclays Bank is to launch contactless credit and debit cards that double up as Oyster travel cards.

www.barclaycard.co.uk

Barclays news release

Transport for London website

Visa UK Plans Contactless Rollout in 2007

MasterCard Announces European Contactless Trials

RBS Says Contactless EMV Trial a Success

Saturday, December 09, 2006

Infineon E-purse - ePayments News

Infineon Combines Contactless E-purse with Access Cards

ThalesThe chip is loaded with e-cash at a loading station and used at locations such as the canteen, food and drink vending machines, coffee machines, and the on-site hairdressers. These locations have been equipped with 140 contactless e-purse payment terminals from France's Thales. The 140 terminals between them process some 10,000 transactions per day, says Infineon. The canteen uses a cash register system from Schaupp along with Thales's AVT.compact payment terminals. Infineon has also installed AVT.compact terminals in food and drink vending machines.

Additionally, one hundred coffee machines have been equipped with the unattended Thales AVT.controller module, Infineon says. The rollout of e-purse technology has been a success, with noticeably shorter waiting times at busy locations such as the canteen's cash registers, Infineon says. More than 90 percent of all staff payments at Infineon's Munich offices are now being made electronically, it says. "In the canteen, we are able to process six payments a minute," Wolf Ruediger Moritz, Infineon's Vice President of Business Continuity, says in a statement. "Even at peak hours, we no longer have substantial queues." Infineon was previously the semiconductor division of Germany's Siemens.

Related Links

www.thalesgroup.com/etransactions

MasterCard, Keycorp Offer Low-Cost Contactless Cards

Europe's Unattended Payment Market Set To Grow

UK's EMV Cards Could Carry An Oyster Application

Japan's E-Cash Market Holds Many Opportunities

Thales

Dec 06 2006 : Chip manufacturer Infineon has implemented a contactless e-purse payment system for 6,500 employees working at its new site in Munich, Germany. Staff have been issued with smart cards which carry both e-purse and security access information on the same Infineon chip, the firm says.

Additionally, one hundred coffee machines have been equipped with the unattended Thales AVT.controller module, Infineon says.

Related Links

www.thalesgroup.com/etransactions

MasterCard, Keycorp Offer Low-Cost Contactless Cards

Europe's Unattended Payment Market Set To Grow

UK's EMV Cards Could Carry An Oyster Application

Japan's E-Cash Market Holds Many Opportunities

Netcash - ePaymentnews

Netcash Launches Digital Currency In UK

CreditmanTo buy Netcash currency, consumers can deposit physical cash at one of the company's partner high street banks or make an electronic transfer from their Internet bank account to Netcash. They can then email Netcash currency to other people, or make a funds transfer from the Netcash Website, the firm says. Netcash claims that the system offers real-time funds transfers for a fee of 1 percent of total transaction value. As no credit cards are used to make online purchases, there is no risk of chargebacks from stolen cards, it says. The system can also handle micropayments, for example media content downloads, according to Netcash In a statement, Netcash says its system has already been implemented by companies4u.com, a UK firm which provides e-commerce services to online merchants.

Netcash also says the Netcash system is accepted by a number of online retailers in the UK. But, in addition to targeting retailers, Netcash wants to encourage consumers to use its payments system on eBay as an alternative to PayPal. Congleton, Cheshire-based Netcash says it is accredited as an e-money issuer by the Financial Services Authority, the UK banking regulator. The firm is run by managing director Paul Tolley and international marketing coordinator Mark Hodkin.

Netcash website

www.companies4u.com

Financial Services Authority

PayPal to Support 10 Extra Currencies

Creditman

Dec 04 2006 : UK start-up Netcash has launched a digital currency system, which it says can be used for both PC and mobile phone-based payments.

Netcash also says the Netcash system is accepted by a number of online retailers in the UK. But, in addition to targeting retailers, Netcash wants to encourage consumers to use its payments system on eBay as an alternative to PayPal.

Netcash website

www.companies4u.com

Financial Services Authority

PayPal to Support 10 Extra Currencies

Friday, November 24, 2006

Visa trails mobile coupons and rewards

Visa USA HQ Trials Mobile Phone Payments

Computer Business ReviewThe San Francisco trial will involve around 500 Visa employees in California. Trial participants will receive mobile payment coupons and rewards via text messages and graphic and bar code images direct to their handsets. According to Visa, the coupons and rewards can be redeemed at on-site cafes located at its corporate campus. Visa says the pilot is expected to lead to larger-scale public trials over the next year which will test both mobile payments and value-added applications.

"With more than 225 million mobile phone users in the U.S. alone, it's only natural for consumer payments to extend to the mobile device," Elizabeth Buse, executive vice president at Visa USA, says in a statement. An online survey carried out by Visa USA recently found that 61 percent of respondents between the ages of 25 and 34 are interested in making mobile phone purchases. The survey also found that over half of US consumers carry their mobile phones at least 75 percent of the time and that 64 percent of consumers are interested in receiving coupons via their mobile handset.

The Atlanta trial, which was launched in December 2005, ended in September. During the trial, 150 Atlanta Thrashers and Atlanta Hawks season ticket-holders with both a Chase-issued Visa credit card and a Cingular wireless phone account made payments at ViVotech contactless readers at concession stands throughout the arena.Also, Atlanta trial participants downloaded content to their Nokia 3220 mobile phones such as ring-tones, screensavers and video clips of favorite players. The Nokia phones were equipped with NXP's NFC chips, Visa says.

Related Links

www.visa.com

www.jpmorganchase.com

www.NXP.com

www.vivotech.com

Issuer-Operator Disputes Delaying NFC Phone Rollout Says Analyst

Visa Offers Contactless Card Toolkit

MasterCard Announces European Contactless Trials

MasterCard NFC PayPass Trial with 7-Eleven and Nokia

Computer Business Review

Nov 21 2006 : Visa USA is to launch a mobile phone payments trial this month at its San Francisco, California headquarters. The pilot follows on from Visa's consumer trial of Near Field Communications (NFC) mobile phone payments at the Philips Arena in Atlanta, Georgia.

The Atlanta trial, which was launched in December 2005, ended in September. During the trial, 150 Atlanta Thrashers and Atlanta Hawks season ticket-holders with both a Chase-issued Visa credit card and a Cingular wireless phone account made payments at ViVotech contactless readers at concession stands throughout the arena.

Related Links

Visa contactless cards - ePaynews

Visa UK Plans Contactless Rollout in 2007

VisaThe rollout will enable cardholders to purchase low-value everyday items, such as their morning coffee and newspapers, by waving a contactless card over a card reader in participating stores, Visa says. The contactless cards will contain EMV chip-and-PIN technology as well as an RFID contactless chip. Cardholders will not be required to enter their PIN for contactless transactions that are under a preset amount. However, if the number of contactless transactions carried out by a cardholder exceeds the card's daily floor limit, the card will need to be swiped in a reader and the PIN entered. "With over 75 percent of all UK cash payments being less than £10 (USD19), the introduction of contactless payments will play a major role in encouraging the use of cards over cash for low-value transactions," Sandra Alzetta, Visa Europe's Senior Vice President, Consumer Market Development, says in a statement. Visa says contactless payments are particularly suited to retail environments such as fast food outlets, newsagents, parking facilities and vending machines, all of which have a high cash turnover and where rapid checkout times are desirable. Research carried out by Visa indicates that UK consumers are likely to appreciate the convenience and speed that contactless cards offer as an alternative to cash, the association says. Visa and its UK members are currently holding discussions with retailers to win their support in advance of the contactless rollout. Further details of the launch plans are expected to be available by March 2007, according to Visa.

www.visaeurope.com

MasterCard Announces European Contactless Trials

RBS Says Contactless EMV Trial a Success

Visa

Nov 24 2006 : Visa UK says its member banks have agreed to roll out contactless cards across Britain, by the end of next year, starting in London.

www.visaeurope.com

MasterCard Announces European Contactless Trials

RBS Says Contactless EMV Trial a Success

Friday, November 17, 2006

NFC on ePaynews.com

Issuer-Operator Disputes Delaying NFC Phone Rollout Says Analyst

Nov 15 2006 : Disagreement between card issuers and mobile operators as to control over payment facilities embedded in Near Field Communications (NFC) enabled handsets is holding back deployment of the technology, says ABI Research senior analyst Jonathan Collins. He tells epaynews that key issues to be resolved are the location of card payment information on the handset, activation of the payment application, and fees payable to mobile operators by card companies.

Nov 15 2006 : Disagreement between card issuers and mobile operators as to control over payment facilities embedded in Near Field Communications (NFC) enabled handsets is holding back deployment of the technology, says ABI Research senior analyst Jonathan Collins. He tells epaynews that key issues to be resolved are the location of card payment information on the handset, activation of the payment application, and fees payable to mobile operators by card companies.

MC's Pay Pass roles out to cabs - ePaynews.com

Philadelphia Cabs Accept Contactless Payment

Nov 16 2006 : VeriFone and MasterCard have announced the first taxicab implementation of 'tap 'n go' contactless cards in the U.S The two companies have installed MasterCard's PayPass contactless payment technology in 250 Philadelphia taxis, along with VeriFone payment systems.

Nov 16 2006 : VeriFone and MasterCard have announced the first taxicab implementation of 'tap 'n go' contactless cards in the U.S The two companies have installed MasterCard's PayPass contactless payment technology in 250 Philadelphia taxis, along with VeriFone payment systems.

Amp'd & Obopay partnership - MoCoNews

» Amp'd Launches Mobile Payments

Related Topics: Amp'd -- Permalink - Comments (1) [by james]

Amp'd has signed up Obopay to offer a mobile payments solution. From the press release: "Amp'd Mobile device users will be able to send money to any mobile phone number and instantly receive money from any Obopay user. The service also comes with an Obopay companion prepaid debit MasterCard that lets users conduct retail transactions at more than 5.5 million retail locations and 396,000 ATMs in the U.S. using their Obopay account funds. With Obopay's account management features, users can also refer friends, check balances, get money owed from other mobile users, and view transaction histories." The two companies are also offering a $25 bonus to people who sign up for an Obopay account.

For me, the interesting part will be when people will be able to send small amounts of money to each other, or a company selling mobile content, without losing a whopping slice of it to the telcos. (Press Release PDF)

Monday, October 09, 2006

Death of the Ringtone - MoCoNews

» The Death Of The Ringtone

Related Topics: Mobile Music, Research, UK -- Permalink - Comments (1) [by jemima]

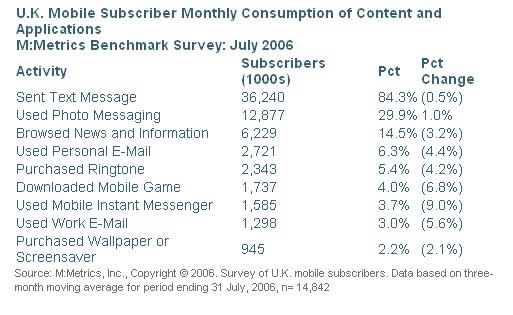

Dodgy sales techniques, piracy and full-track downloads are all being blamed as the bottom falls out of the ringtone market. Research by MusicAlly tracks UK ringtone sales growing from £34.8 million in 2000 to £177.3 in 2005, but predicts that will fall to £143.5 million this year and £78.8 million by 2007.

It's quite understandable though: the kids don't see the point in paying £3.50 for a tinny 10-second ringtone interpretation of a new song when they can often copy the full MP3 onto their phone and set that as their ringtone. That's not always done legally though - this piece says younger phone users are using their phones to record music on their computers or are Bluetoothing tracks from friends. There's also software floating online that converts MP3s to ringtones.

Misleading sales subscriptions are also a factor because users often don't trust ringtone services.

M:Metrics data for Europe shows a 42 percent drop in sales, part of what senior analyst Paul Goode described as a significant shift for the ringtone market: "As mastertones supersede polyphonic tones, and short codes gain steam as a merchandising vehicle, the economics of the business will have to change. The availability of tools to make user-created ringtones more accessible to the masses poses an even greater threat to companies who can offer no additional value to a consumer who buys a ringtone in lieu of making one themselves."

Related: UK Leads In Mobile Music Consumption, US In Ringtones

– Mobile TV Now More Successful Than Ringtones -- Vodafone

SonyBMG on Mobile Music - MoCoNews

» Sony BMG Bullish On Mobile Music

Related Topics: Mobile Music, Research, SonyBMG -- Permalink - Comments (0) [by james]

A couple of interesting points about digital music as part of Sony BMG's business...it's currently around 20% but "that percentage should rise "significantly" when someone figures out how to make platforms interoperable. Hesse expects digital revenue to rise between 50 percent and 60 percent in 2006?.

On the mobile side: "On average, 4.1 million, or 2.1 percent of the 190 million U.S. cellular subscribers, used their mobile phone as a music player in August, according to M:Metrics Inc. The research firm estimates that number slides in Europe to 649,490."

Related stories:

–UK Leads In Mobile Music Consumption, US In Ringtones

Microsoft Points on Seeking Alpha

Microsoft's Latest Marketing Scheme: Pinching Pennies Off the Customer

Largely unnoticed in the pricing announcement last week was this little tidbit about how consumers might pay for Zune music. CNET had a pretty decent description in their article, where they accurately noted that Microsoft's real play is to get people to buy subscriptions for $14.99 a month. But if pressed, they'll generously allow people to buy individual songs. But you can forget one-click buying; Microsoft (MSFT) has a cuter idea:

There will also be the option of purchasing individual songs through a system called Microsoft Points. The new Microsoft cash system will work by adding money to an account, as with a prepaid phone card. Points will then be deducted from the account with each purchase. A single song will cost 79 points, "the equivalent of 99 cents," according to Microsoft spokeswoman Kyrsa Dixon.

The point system is already used in the Xbox Live Marketplace, and Microsoft plans to host other online stores where Microsoft points can be redeemed, according to Katy Gentes, product marketing manager for Zune. In the United States, points are available in denominations of $5 for 400 points, $15 for 1,200, $25 for 2,000 and $50 for 4,000. That makes $1 worth about 80 points.

Now from a marketing point of view, there are two marketing tricks going on here. First is the concept of not having 100 points equal a dollar. That would be too simple and easy to understand. Instead, Microsoft sets the song price to 79 points, which most people will perceive as being inexpensive because it is less than 99. Cute, very cute.

The second marketing trick is the use of a new form of currency; yes, Microsoft money has finally arrived, and it has all the charm of an end user licensing agreement -- and just as many tricky parts. Note the denominations offered above and think about this common transaction: buying your average, garden-variety album for $9.99. You'll need probably 799 points to buy that. But notice that there's no 800 point denomination. Microsoft is betting that most consumers won't buy two 400 point packs, but will instead opt for purchasing 1,200 points for $15, and will leave the extra 400 points on account with Microsoft. So consumers end up either 1) doing extra work to pay exactly the right amount (i.e., going to the store, purchasing two 400 point packs, returning to the music purchase and then buying their album), or 2) provide an interest free loan to a company that has $40 billion in the bank. Cute, too cute by half.

Microsoft seems to take particular glee in making consumers work harder than necessary to buy their products and grabbing every fraction of a penny they can squeeze out of the transaction. If the company spent half as much effort investing in, say, making a truly elegant hardware device (instead of just re-badging someone else's) and making the user experience simple and hassle-free with one-click credit card payment (it worked for Amazon (AMZN), didn't it?), they'd probably make more money in the end than pinching pennies with tricky pricing and proprietary money schemes.

Someone once said that the lottery is a tax on people who are bad at math. Maybe Microsoft intends Zune Marketplace to be a tax on people who like marketing tricks. It might work, but it's no way to build customer loyalty.

Full disclosure: I own shares of Apple Computer.

PayPal in court

Making PayPal Your Friend

Ron Lieber writes for the Wall St. Journal about PayPal and some recent changes following settlement of complaints brought by 28 state attorneys general. Lieber recommends not funding PayPal transactions directly from your bank account account but, rather, using either a debit card linked to your checking account or selecting the credit card option each time you use PayPal.

Friday, October 06, 2006

Valista survey on Operator's cut

|

Everyone in the content game knows that the mobile industry’s biggest bugbear is the large slice of revenues that network operators take. Now its official. Research carried out last week at Mobile Content World in London of the exhibitiors and delegates found that more than half of respondents correctly answered that mobile operators currently take 40 to 50 per cent of mobile content transactions. However, less than six per cent believe this will be the case in three years time. In fact almost two-thirds of those questioned believe that in three years' time, mobile operators should cut their share by at least half — to less than 20 per cent, with 18 per cent of respondents believing that they should take only five per cent.

The study, carried out by Valista a leading, independent provider of merchandising, payments and settlement solutions, finds that what is clear is that in order to safeguard revenues, the industry needs to drive the uptake of mobile content through creative and flexible pricing, content bundling and promotions and cleverly targeted content.

More than 28 per cent of delegates surveyed believe that targeting content by demographic groups and communities will be the most likely way to increase content purchasing, closely followed by flexible pricing (27%) and improved mobile search (20%).

According to Arlene Adams, Vice President at Valista who attended the Mobile Content World show yesterday, "Currently, operators take the greatest share of mobile content revenue, but the distribution of power could shift - particularly when the major media moguls secure their foothold in the marketplace.

Consolidation and the entrance of major consumer brands will shape the future value chain, and operators need to balance recouping revenues with the desire to maximise their share in the long run. In this regard, operators need to look at more innovative merchandising and marketing tools to encourage their consumers to buy more. In addition, a payments model which lowers or eliminates revenue leakage and allows end-to-end traceability for transactions and the parties involved, will allow operators to look at lowering their fees while encouraging growth in the content market."

Good news for the industry came in the finding that mobile TV and Video downloads will be the most popular forms of content over the next few years, an opinion that mirrors recent analyst predictions. Broadcasting rich content will see a move from lower value payments (micro-payments) to higher value transactions (macro-payments). In this regard, operators need to protect their brand and look at personalised and compelling content to grow Average Revenue Per User (ARPU) and drive off competition from more traditional payment schemes. Less positive for operators was the finding that only 15 per cent of content purchased will be part of an ongoing subscription model.

What may make uncomfortable reading is the fact that, according to attendees, mobile operators will not see content purchases making up for falling revenues. More than half of those who contributed (58%) believe that in three years' time, less than 25 per cent of total operator revenue will come from mobile content and 15 per cent believe that it might drop as low as 10 per cent. This figure is interesting given that mobile content and entertainment services market accounted for less than four per cent of total mobile service revenue and less than 19 per cent of non-voice revenue in 2005 according to research firm, Analysys. Another figure quoted by iGillott Research predicts that mobile content will account for 40 per cent of operators' revenue by 2009.

Despite the variations in the predictions above, those questioned in the Valista poll were in agreement on the future of mobile payments, with more than 65 per cent believing that the current system of paying for mobile content via Premium SMS will, in the next few years, give way to more flexible and robust payment methods such as paying via the monthly bill (direct-to-bill charging).

Today's Payments News

Mobile Contactless Payments - $36 Billion In Payments By 2011

Strategy Analytics has released “Mobile Contactless Payments –Growth on the Horizon,” analyzing payment for goods or services using phones instead of cash or credit/ debit cards. According to the company, "the report concludes that the conditions are finally right for growth over the next five years, projecting that mobile contactless payment will be used to drive sales of $36 billion by 2011."

Will Contactless Payment Cards Connect In The U.S.?

Bankrate's Gregory Taggart reports on the growth in contactless card usage in the US - highlighting Visa data showing that "contactless transactions are an average of 25 percent faster than cash" and claiming that the contactless roll-out in the US has been the fastest deployment of new payment technology ever.

UK: HSBC Rings In Mobile Banking

Richard Wray reports for The Guardian about HSBC's launch today of a new mobile banking service that will allow customers to "use their mobile phone to check their bank balance or help their friends or family pay for calls." According to Wray, "after downloading a simple piece of software to their phone, the bank's customers will be able to check their balance or find out if they have been paid, wherever they are."

- NTV, NTT DoCoMo Co-develop Mobile Phone System to Distribute and Store Video-embedded E-coupons and E-cards

- Hypercom Wireless Payment Terminals at Arizona State Fair Let Fairgoers Use Credit/Debit to Pay for Rides

- MoneyGram Delivers New Patent-Pending Technology Allowing Billers to Review Payments Online Prior To Acceptance

- National Bankcard Systems Selects WAY Systems Mobile Transaction Terminal as Preferred Wireless POS Payment Solution

Thursday, October 05, 2006

Youth & Texting - from 160 Characters

| News: U TXTING 2 ME? | ||

|

Wednesday, October 04, 2006

Mobile banking UK - Payment News

HSBC, First Direct launch mobile banking

HSBC and First Direct are going live with their mobile banking service in the U.K. today, which runs over GPRS and is available to 02, Vodafone, Orange, T-Mobile, Virgin and Tesco subscribers. The new service enables users to access their bank accounts for mini-statements, balance inquiries and to top off their phone accounts. The companies say the service will result in a cost savings for the users because it will save them on ATM fees from rival banks.

For more on the mobile banking service:

- see this article from VNUnet

Tuesday, October 03, 2006

Bitpass on Payments News

Bitpass Unveils Next-Generation Digital Commerce Engine

Bitpass has announced its next-generation digital commerce engine, which the company says "allows merchants, publishers, marketers and consumers to fully capitalize on digital content."

Norway: BankID for Mobile Phones

Norway: BankID for Mobile Phones

Telenor and the Norwegian banking industry have announced they have entered into a "unique agreement to make life simpler for millions of Norwegians by making banking and payment services available via a mobile phone, anytime and anywhere."

The Norwegian banking industry, through the Norwegian Savings Banks Association and the Norwegian Financial Services Association (FNH), is behind the BankID Partnership (BankID Samarbeidet). The BankID Partnership has developed BankID, an electronic proof of identity which can be used for identification and signing agreements on the Internet.

BankID for mobile phones builds on the cooperative model in the BankID Partnership. The agreement between Telenor and the BankID Partnership is unique as there is no equivalent cooperation between the banking industry and the telecommunication sector in other countries.

"With BankID for mobile phones, we are helping simplify our customers' lives, while at the same time participating in a unique and innovative partnership with the banking industry," says Berit Kjoell, Division director in Telenor.

BankID for mobile phones strengthens BankID's position as the most widespread and widely used electronic proof of identity. Telenor is the first operator to enter into an agreement with the BankID Partnership, but this does not exclude other operators from signing a similar agreement.

BankID for mobile phones will be available in 2008 and all banks participating in the BankID Partnership may offer BankID to their customers. When that happens, 2.3 million Internet bank customers and 2.7 million Telenor subscribers will be able to identify themselves and sign agreements using a mobile phone. This means that customers decide the bank's opening times and have access to new services they need -- secure services, anytime and anywhere.

"The financial industry is at the forefront of using modern and cost-effective solutions to the benefit of people in general. BankID for mobile phones can help meet people's expectation of being able to satisfy their banking needs anytime and anywhere. Having to stand in line to pay bills is ancient history," says Arne Skauge, Managing Director of FNH.

Usage of mobile phones has gone beyond speech and SMS to areas such as MMS and the Internet. BankID for mobile phones is a natural part of this development, and will initially be used in four areas: logging on to Internet banks, mobile banking, electronic service for business and the public sector, and account-based payment services for the Internet and mobiles (BankAxess).

The BankID Partnership was set up by the Norwegian Financial Services Association (FNH) and the Norwegian Savings Banks Association to develop and coordinate infrastructure for the entire banking industry. The banks participate directly in the BankID Partnership through projects and involvement in working groups. Each bank issues BankID and supplies the market with accompanying services.

Thursday, September 28, 2006

News Corp President in Silicon News

News Corp utters mobile content battle-cry

"No one needs our content but we've made them desperately want it"

Published: Thursday 14 September 2006

Chernin said today only four per cent of the 219 million mobile subscribers in the US watch mobile TV on their handsets. But if that figure increased to 20 per cent and each viewer spent just $10 per month on mobile video, mobile TV would generate nearly $5bn in revenue.

Getting every teenager in America to spend $5 per month on mobile entertainment could generate another $5bn for the industry, Chernin said. And simply increasing the number of people buying ringtones by just five per cent could generate $1bn revenue per year, he said.

Read the whole article

Monday, September 25, 2006

MoCoNews coverage of Mobile Content World

| |

| |

| |

| |

Friday, September 22, 2006

PayPal micro payment rates

PayPal introduces micropayments pricing scheme

Online payments firm PayPal is cutting the processing fees it charges merchants for low cost digital purchases such as ringtones, video games, online greeting cards and music downloads.The eBay subsidiary says its new micropayments pricing scheme is designed to enable customers to purchase low cost digital items without having to sign up for annual subscriptions or pre-funded payment accounts.

The new pricing is designed especially for payments less than $2. Under the new payments structure merchants will be able to process payments at a rate of five per cent plus five cents per transaction. PayPal says the new fees mean that merchants will pay 40% to 60% when processing low-cost payments, compared to the industry's current payment processing rates of two per cent plus 20 to 30 cents per transaction.

Peter Ashley, director of PayPal's micropayments business, comments: "With our new pricing tier for digital goods, merchants can affordably provide customers with what they are demanding - the opportunity to purchase the content they want without the need to sign up for subscriptions or pre-payments."

Merchants can opt for the new pricing structure or stay with PayPal's existing system. The firm's standard, volume-based transaction fees range from 1.9 to 2.9%, plus 30 cents per transaction.

More than 14 million US consumers purchased digital content costing less than $2 in 2004, an increase of over 10 million from 2003, according to research by micropayments firm Peppercoin and Ipsos-Insight released late last year.

Thursday, September 21, 2006

text-based businesses at Payment

Remote Order And Pay Redux

Sarmad Ali writes for today's Wall St. Journal about how SMS-based text messaging is the latest way consumers are ordering their morning coffee (and more) while in-bound to the office. Ali writes about New York-based Mobo Systems, Menlo Park-based MyTango, and UK-based Software For Restaurants and their different flavors of remote order and pay. Several years ago, a Seattle-based company named Ontain pioneered remote order and pay services (using a simple IVR approach instead of SMS-based text messaging) and conducted several trials in various markets with, among others, Starbucks. Ontain's approach failed to achieve commercial success, however, and likely was one of those cases of being ahead of its time.

Wednesday, September 20, 2006

Today's Payment News

PayPal: The Good, The Bad and The Ugly

Rich Brooks of flyte new media blogs for MaineToday.com about PayPal, its good, not so good, and "ugly" attributes. Brooks concludes that "for many people the flexibility and simplicity PayPal offers is too good not to consider. Although it may not be right for everyone, it's an inexpensive, effective tool for many."

Yodlee Announces BillPay Account Accelerator

Yodlee has announced the Yodlee BillPay Account Accelerator, a new service that "removes the hassles of canceling an existing bill pay service and setting up payments all over again with a new bill pay provider." Yodlee also says that the service "frees the 40+ million online bill payers to choose the service that’s best for them, and enables financial providers with differentiated bill pay services to capture a greater share of the fast growing bill pay market."

NFC Turns Phone Into A Wallet

David Carey reports for EE Times on how a "near-field communication device turns a Nokia cell phone into a practical tool in commercial and industrial settings for tracking assets, transmitting small data files or even auto-launching various phone-based tasks or requests" - and that "NFC technology has the ability to support what may be the most compelling application of all: a wallet in your handset."

Tuesday, September 19, 2006

The Reg on NFC

The NFC revolution is running late

Not going to change the world...yet

Published Tuesday 12th September 2006 13:51 GMT

Paypal again

Mowave Uses PayPal's 'Text to Buy' Service With Magazines

UK-based mobile entertainment and solutions provider Mowave has launched a new mobile service with PayPal that will allow readers of Maxim and Stuff magazines to purchase a range of products, such as subscriptions and electronics, simply by sending a text message from their mobile phone. The service, which utilizes PayPal’s new “Text to Buy” platform, marks the first time that UK publications have implemented a mobile payment system to process subscriptions or purchases of goods.

Monday, September 18, 2006

Great off-deck Payments article at Fierce Mobile Content

How A Payments Platform can Bridge the On/Off-Deck Divide

By Raomal Perera, CEO, Valista

With increasing demand for off-deck content today, content and service providers need to provide consumers with an easy-to-use solution for purchasing a variety of digital content and services through any mobile device. By 2007, the mobile premium content market is predicted to contribute to over 25 percent of global mobile revenue. With off-deck sales already dominating European mobile commerce, reaching between 40 to 70 percent of total revenues and with North America rapidly catching up, operators can no longer limit themselves to offering content through their own portal. A combined on-deck and off-deck strategy needs to be established.

Historically, operators were reluctant to provide access to off-deck content because of the fear that brands would suffer from poor customer service, unsanctioned transactions and fraud by third parties. While content providers prefer to stay off-deck, the ability to establish a presence within an operator's portal increases its access to subscribers--increasing sales, lessening credit risk and allowing for faster settlement. Operators also face business and technical challenges in managing the complexities of incorporating third party content and providing effective, cost-efficient transaction services outside of their existing billing systems.

Support for business processes such as payment processing, customer care, fulfillment, exception handling and settlement are vital components to bridge on and off deck business strategies.

Direct-to-Bill Charging

Premium SMS (PSMS) has been the primary method used by content providers to allow the purchase of off-deck content. However, the need for greater visibility into transactions is definitely a key factor in successfully providing off-deck content to subscribers. While PSMS as a billing method has been used in the past, it has limitations that are of concern to all parties involved in the transaction. The PSMS transaction process does not include credit checks, fraud protection or visibility into the transaction for all parties involved. Security and revenue leaks are of primary concern to both third-party content providers and operators. A Direct-to-Bill charging service provides a more robust payment mechanism when compared to PSMS. Using a Direct-to-Bill service that leverages a payments platform, merchants are able to charge consumers more accurately and to provide appropriate security, fraud protection and transparency into transactions for all parties.

Revenue Sharing

As the operator creates more highly innovative marketing offers, these programs have a direct impact on the revenue-sharing contracts that it holds with content providers. This creates the need for operators to have a system capable of ensuring revenue assurance and proper settlement for all parties involved in the transaction.

For example, if a new Spiderman movie comes out, a game, wallpaper, ringtone, and other ancillary products may be combined by a mobile operator to create a bundled offer. The discounting of products is implicit in their bundling into a single offer. Who bears the cost of this discount in the revenue-sharing relationship? If the operator offers a 20 percent discount on the bundle of a wallpaper, a ringtone and a game because it will drive purchases, it is important to highlight which suppliers are willing to sponsor a portion of that discount, or if sponsorship of the discount will fall solely on the operator's shoulders.

For a successful revenue sharing model, mobile operators and content providers need the freedom to define their contracts, without being constrained by a technology's ability to support them. A payment platform with revenue sharing technology will enable service providers and merchants to guarantee accurate and timely transaction settlements covering terms such as payments, payment schedules, discount sponsorships, liability for exceptions, refunds, non-payments, cancellation fees, and fraud. This ensures that the revenues and costs are distributed to the correct parties per the contractual arrangements.

Conclusion

As the premium mobile content market continues to grow, a more collaborative payment mechanism is needed, enabling content innovation and offering new opportunities for promotional programs, joint discounts, and loyalty programs. Similar to an e-commerce platform, mobile operators need to link their offerings with the generation of accounts receivable, accounts payable and settlement for multiple parties. In order to do so, operators need a comprehensive payments platform to support their on-deck and off-deck businesses. Payments platforms provide the key technology that allows operators, ISPs and aggregators to work together to successfully exploit both on-deck and off-deck markets--simultaneously. The successful and proper deployment of payments solutions helps operators, aggregators and content providers grow while still focusing on their core competencies. With the appropriate billing and payments platform, consumers will be able to access more interesting content, allowing content providers and operators to increase revenues, thereby creating a win-win-win situation for all players in the mobile content ecosystem.

Friday, September 15, 2006

UK Cash habits - Payments News

APACS Publishes The Way We Pay For UK Cash, ATMs

APACS, the UK payments association, has published a new report titled "The Way We Pay: UK Cash and Cash Machines" reporting that the number of UK cash machines has more than doubled in the past six years (from 27,379 in 1999 to 58,286 in 2005) and that Britons make the largest number of cash machine withdrawals of any country in the EU, some 2.7 billion transactions in 2005, or more than 42 per person.

Thursday, September 14, 2006

Sports scenarios start to scale

| Sports fans enthuse about NFC & mobile payments |

|

| | |

| The NFC/mobile payment trial at the Philips Arena in | |

http://www.thewisemarketer.com/briefs/archive.asp?action=read&bid=1970

Subscribe to:

Comments (Atom)